Job Market Conditions Remain Dire

The June 2020 Bureau of Labor Statistics jobs report (that is, the Employment Situation news release) shows that as of mid-June, U.S. labor market conditions showed continued partial rebound from the depth of the shutdowns in April. This post presents my quick parsing of the report. A later post will examine differences by gender and race.

In March, I published a post on why the jobs reports are so influential and what indicators I track to understand the impact of COVID-19. Also see subsequent updates for April and May. I do not repeat that background here.

- Data quality is good. Again, the Bureau of Labor Statistics reported no new data quality issues, even though putting together the report was challenging. The bureau’s accompanying note documents methodological issues encountered and how it managed them.

- Integrity: After May’s partial rebound, some observers voiced fears that the data were tainted. Fortunately, the practices, laws and directives that protect the integrity of Bureau of Labor Statistics’ data continue. I see no indication of any attempt, successful or not, to manipulate these data. See my explainer about bureau data integrity practices.

- Misclassification in the household survey: Since March, the Bureau of Labor Statistics has noted that the true unemployment rate is likely higher than the official rate because many workers who respond that they are employed but not at work are really on temporary layoff. See questions 7-14 of the note and my previous discussion. This problem persisted in June, albeit much abated. By my admittedly crude estimate, the likely rate of misclassification has now fallen to 16 percent of people on temporary layoff, from about 39 percent in March. The bureau is clearly working actively to reduce this problem going forward.

- Response rates: Pandemic-related disruptions further reduced response rates for both surveys. Household survey response rates of 64.9 percent in June showed further deterioration from the previous average rate of 82.5 percent (for the 12 months ending in February 2020). Payroll survey response rates for the first preliminary release (65 percent) also slipped further below normal (see questions 1 and 4 in the bureau note). Thanks to their extraordinary efforts, bureau staff attained response rates sufficient to meet their quality standards. However, the continuing decline in response rates is of concern going forward.

- The labor market slump is still very deep, even with the consequential rebound achieved in May and June.

- Payroll jobs increased by 4.8 million in June, which represents 22 percent of the 22.1 million jobs lost from in March and April. This is, by far, the largest one-month job gain in the history of the payroll survey. Added to the rise in May, 34 percent of COVID19-related job losses were regained by mid-June. While April’s losses were remarkably widespread (96 percent of industries lost jobs), the gains in May and June were less so: 64 and 75 percent of industries recouped some jobs, respectively.

- The official unemployment rate declined by 2.2 percentage points to 11.1 percent. The bureau estimates that had there been no misclassification, the seasonally adjusted unemployment rate might be as high as 12.3 percent and would have declined by 4.1 percentage points from May. So, the misclassifications lead to understating both the severity of current conditions and the size of June’s rebound.

- The employment-to-population ratio rose from 52.8 to 54.6 as some workers returned to the labor force, although it remains far below February’s ratio of 61.1.

- The labor force participation rate, which was 63.3 percent in February, regained 0.7 percentage points, reaching 61.5 percent.

- The labor underutilization rate “U6” declined from 21.2 percent to 18.0 percent. In February, the U6 was just 7.0 percent. U6 is the broadest of the agency’s labor underutilization measures. U6 counts all workers who are unemployed or working part-time involuntarily, plus people who have left the labor force, but still want a job and have looked for one or worked during the last 12 months as underutilized.

- My COVID-19 disruption table adds up six distinct ways the crisis has disrupted (suspended or curtailed) the jobs in the U.S. labor market. I use it to track the rebound and the status of the remaining disrupted workers.

- The indicators. Since disruptions can take many forms, I track these indicators:

-

- Employed workers not at work—workers on leave from their employer, whether paid or not (for illness, family reasons, vacation, etc.—the bureau believes that many of these are misclassified workers actually on temporary layoff, see the bullet on misclassification above).

- Workers part-time for economic reasons—workers who prefer to work full-time but only found a part-time job or who usually work full-time but had their hours reduced by their employer

- Unemployed workers on temporary layoff (furloughed)—laid-off workers who expect a recall

- Unemployed workers not on temporary layoff—includes workers permanently laid off, new and re-entrants and job leavers

- People out of the labor force who currently want a job—people without a job who are not looking for work but say they want a job

- People out of the labor force who do not want a job—largely students, retirees and people with disabilities or caring for family members

-

My measure of COVID-19 disruptions is simply the change in the number of workers in each category since February. The first three categories capture workers whose relationships with an employer are intact despite disruptions, in contrast to the latter three. See here for why that matters. (Note for wonks: I use seasonally unadjusted data, for comparability.)

- May to June rebound. By this metric, the number of disrupted workers declined by about 6.7 million in June. The first two columns of the table show how much June’s rebound affected each type of disruption. Interestingly, almost two million workers joined the ranks of the unemployed who are not on temporary layoff. The rise in this category reflects more people actively looking for work in June. Some may be returning to the labor force from the sidelines, others may be newly laid-off and others’ previously temporary layoff may have become permanent.

Most of June’s rebound took the form of 4.4 million fewer workers on temporary layoff. This likely reflects the ease of recalling workers from temporary layoff, aided in some cases by the Paycheck Protection Program. Less positively, it can also result from the conversion of temporary layoffs to permanent ones.

The other sizable improvement was in the number of people out of the labor force who said they did not want a job. Interestingly, in both May and June, this segment declined much more than the category of people who said that they want a job.

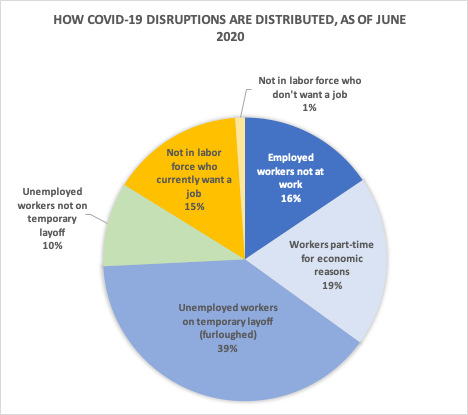

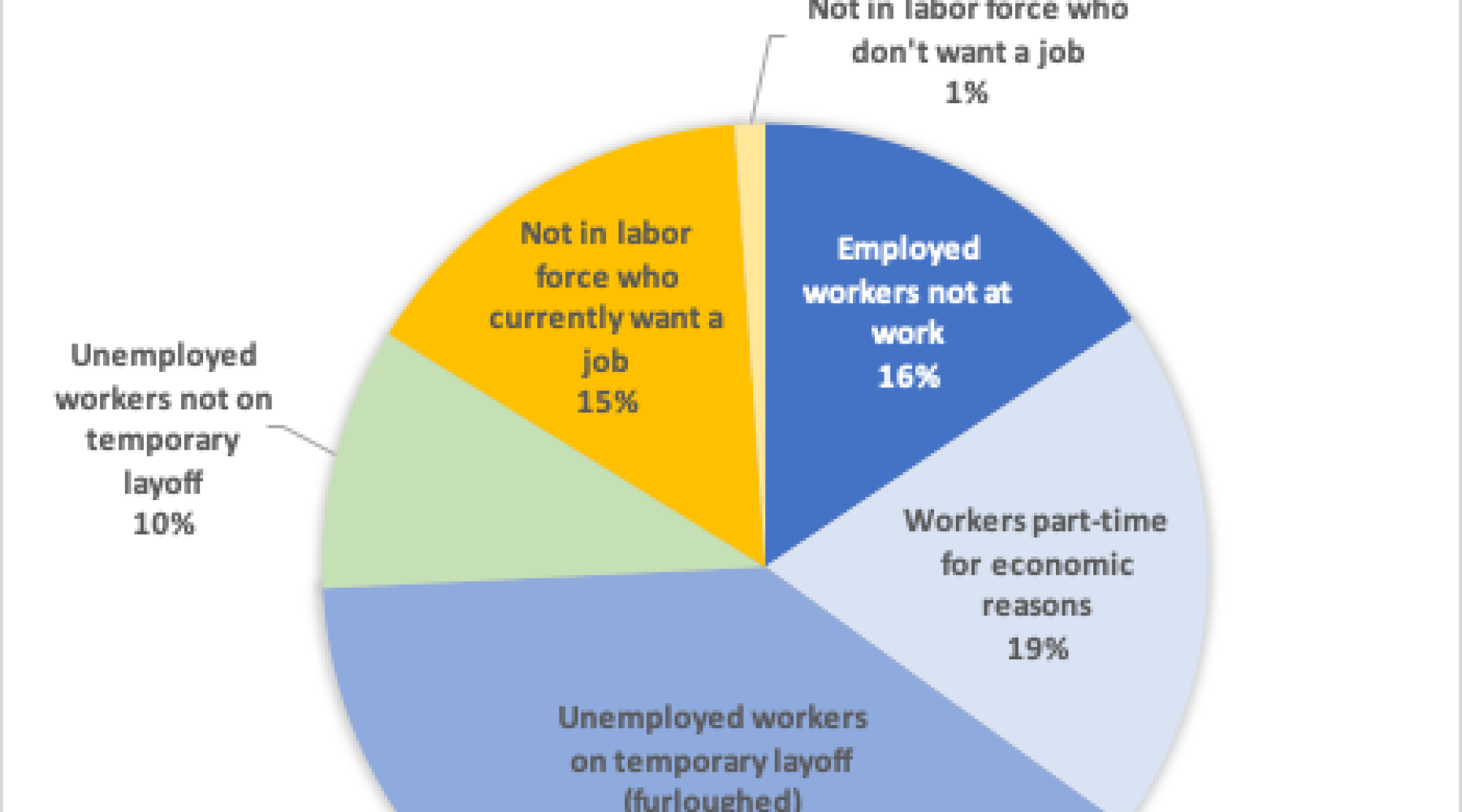

- Ongoing disruptions. The third and fourth columns of table show that in June, COVID-19 was still disrupting the jobs of over 24 million workers (about 15 percent of the labor force in February). The pie chart shows the percentages in the fourth column of the table.

Of those still disrupted, 39 percent are on temporary layoffs (furloughs). Another 16 percent were employed but not at work, which includes business owners who are shut down, misclassifications of workers on temporary layoff and other unusually high use of leaves from work. Another large group (19 percent) is working short hours. In all, 74 percent of disrupted workers maintain a tie with an employer. These are shown in the blue slices of the pie chart.

The share that are unemployed with no connection to an employer climbed to 10 percent of disruptions in June. And in contrast to April, almost all of the COVID-19-related increase in those out of the labor force now consists of people who said they do want a job. Their share of disruptions is 15 percent, compared to the 1 percent who do not want a job.

- Implications for the future

In the best-case scenario, April will turn out to be the job market trough of the COVID-19 downturn. That is, subsequent reports will show declining unemployment rates and further job growth. Why would it be the trough? Since May, states have phased out many restrictions, allowing more workers to return to work. Furthermore, substantial Paycheck Protection Program funds went out in May, funding the recall of many workers.

Even if April was the trough, we are far from assured of a rapid recovery. The high share (74 percent) of maintained relationships with employers should be help speed the recovery when restrictions are lifted, particularly early in the recovery. Yet, much could go wrong.

Risks from renewed virus infections, more civil unrest or lack of fiscal policy support could derail or slow the nascent recovery. June’s unemployment rate is higher than at the trough of the Great Recession. Many states may soon need to forestall or reverse reopening steps. Furthermore, most provisions of the CARES Act will expire soon. Initial unemployment insurance claims tell us that layoffs were still high throughout June, so those are increasingly likely to be recession fallout, rather than direct impacts of the COVID-19 shutdown. Confidence, investment and spending will take time to restore. Even employers who intended to recall their workers may go bankrupt instead of reopening or may need to adopt a new business model with different staffing requirements.

In sum, after two months of rebound, job market conditions remain dire and downside risks are high. Thus, policy will be very important to help support as robust a recovery as possible.

| Type of job disruption | May to June change | Remaining disruptions: February to June change | ||

|---|---|---|---|---|

| Thousands of disrupted workers | Share of change | Thousands of disrupted workers | Share of disrupted workers | |

| Employed workers not at work | -413 | 6% | 3,779 | 16% |

| Workers part-time for economic reasons | -1,123 | 17% | 4,706 | 19% |

| Unemployed workers on temporary layoff (furloughed) | -4,438 | 66% | 9,527 | 39% |

| Unemployed workers not on temporary layoff | 1,996 | -30% | 2,327 | 10% |

| Not in labor force who currently want a job | -789 | 12% | 3,660 | 15% |

| Not in labor force who don't want a job | -1,962 | 29% | 268 | 1% |

| Total disrupted | -6,729 | 100% | 24,267 | 100% |

| Share of February labor force (164,235) | 4% | 15% | ||